2025 was a big year for tax legislation changes, with the One Big Beautiful Bill (OBBB) being signed into law in July 2025. While many provisions of the 2017 Tax Cuts and Jobs Act were extended, there are a few new provisions that open the door to new planning opportunities for realtors.

In this article, we’ll cover a brief overview of what existing provisions were extended and go into detail on new strategies that you can take advantage of going into the next filing season.

Extended TCJA Provisions

Many of the provisions in the 2017 Tax Cuts and Jobs Act (TCJA) were set to expire over the next few years. The One Big Beautiful Bill extended a few key provisions that impact realtors, including:

- Qualified Business Income Deduction – The QBI deduction was extended, meaning realtors can still deduct up to 20% of net income off their tax bill.

- Tax Rates – The tax bracket thresholds and percentages were reduced under the TCJA. These brackets were extended under the OBBB.

- Standard Deduction – The TCJA eliminated personal exemptions and nearly doubled the standard deduction. The higher standard deduction thresholds are still in place and adjusted for inflation each year.

While these aren’t new provisions, they are impactful to your tax situation and an important component of planning for 2025.

Leverage Bonus Depreciation

One of the most impactful components of the OBBB for realtors is the reinstatement of bonus depreciation. Under the TCJA, bonus depreciation began to phase out. In fact, the 2025 bonus depreciation rate was set to be 40% for 2025. Now, purchases made after January 19, 2025, can take 100% bonus depreciation.

While Section 179 is still in place, the deduction is limited for vehicles. However, you can now leverage the 100% bonus depreciation threshold to immediately expense new vehicles purchased in 2025, which can be a huge write-off. If you’ve been putting off the purchase of a new vehicle, now might be a great time to buy to save money on your 2025 tax bill.

Deduct Car Loan Interest

Another new deduction that realtors can leverage from the OBBB is the car loan interest deduction. Between 2025 and 2028, certain car loan interest is deductible. The loan must have originated in 2025, the vehicle must be new, and the final assembly must have been in the United States. The deduction is limited to $10,000 per year and phases out when your Modified Adjusted Gross Income (MAGI) exceeds $100,000 for single filers and $200,000 for joint filers.

It is important to note that car loan interest related to your business is a normal business deduction; however, this new deduction will come into play if you have a mixed-use vehicle. Let’s say that you use your vehicle 70% for business purposes and 30% for personal purposes. Your total car loan interest for the year is $5,000. In this example, $3,500 of your car loan interest would be deductible as a business expense and the remaining $1,500 would qualify for an additional deduction.

Like past tax years, the IRS does not allow you to double-dip on your vehicle expenses. This means that if you take a mileage deduction, you will not be able to deduct other expenses, like gas and car loan interest. Working with your tax accountant is the best way to determine which route is best for your tax situation.

Maximize Itemized Deductions

In past years, state and local taxes (SALT) have been limited to a deduction of $10,000. The OBBB increases this threshold to $40,000, which may mean that itemizing your deductions can be more advantageous compared to taking the standard deduction. For reference, the 2025 standard deduction is $15,750 for single filers, $23,625 for head of household filers, and $31,500 for married filing joint taxpayers. The increased SALT limit begins to phase out once your MAGI exceeds $500,000.

With the new SALT limit, maximizing itemized deductions can be a favorable tax strategy. Mortgage interest, charitable contributions, investment interest, and medical expenses above 7.5% of your AGI are all reported on Schedule A with your state and local taxes.

The increased SALT threshold also draws in new considerations for pass-through entities. In recent years, pass-through entities have started paying taxes at the entity level to bypass the $10,000 SALT cap. Now, it may make more sense to pay taxes at the individual level and itemize your deductions. This decision is highly personal, meaning it might make sense in one year and not the next. Talking with a qualified tax preparer will be the best way to determine which route you should take.

Other Planning Strategies

While bonus depreciation, car loan interest, and the SALT threshold were the main changes applicable to realtors in 2025, there are other planning strategies that are still beneficial. Let’s briefly cover a few of these strategies:

- Maximize Deductions – Remember, all expenses related to your real estate business can lower your taxable income. Think advertising, travel, insurance, bank charges, and more. Keeping track of these expenses will help you lower your tax bill.

- Consider Health Insurance – Most realtors will find health insurance through the marketplace. Expenses paid toward health insurance premiums are deductible.

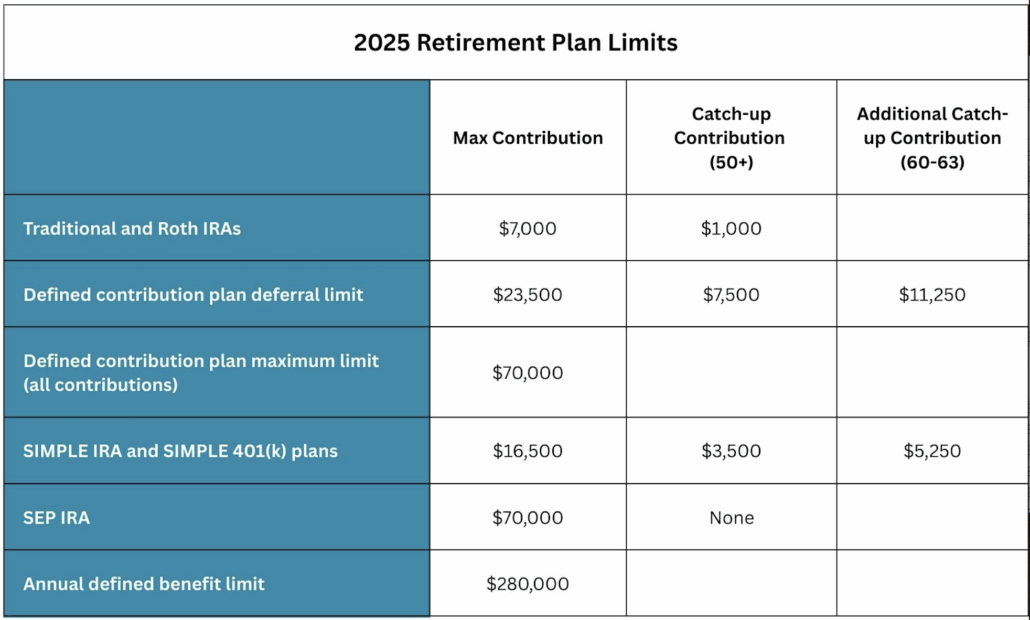

- Make Retirement Contributions – Retirement contributions, such as to IRAs or 401(k)s, can lead to credits and deductions. Even if you are years away from retirement, making these contributions now can be beneficial to unlock tax-advantaged growth and lower your taxable income.

- Revisit Entity Structure – If you are operating as a sole proprietor or a single-member LLC, it might make sense to convert to an S Corporation to minimize self-employment taxes. Reach out to a tax professional to go over whether this strategy is right for your business.

- Time Income – Towards the end of the year, it can be beneficial to time income and expenses. For example, you might expedite payments so they are dated December while holding off on depositing a check until January. Timing income and expenses is only beneficial if you use the cash basis of accounting, which is used on Schedule C.

Summary

How can you save money on your tax bill this year? Tax planning now is more important than ever, especially following the passage of the One Big Beautiful Bill. For any tax-specific questions, contact your tax preparer.