Here are the answers to ten common donation, meals, and gifting expense questions, updated for 2026. If you have any follow-up questions, don’t hesitate to reach out.

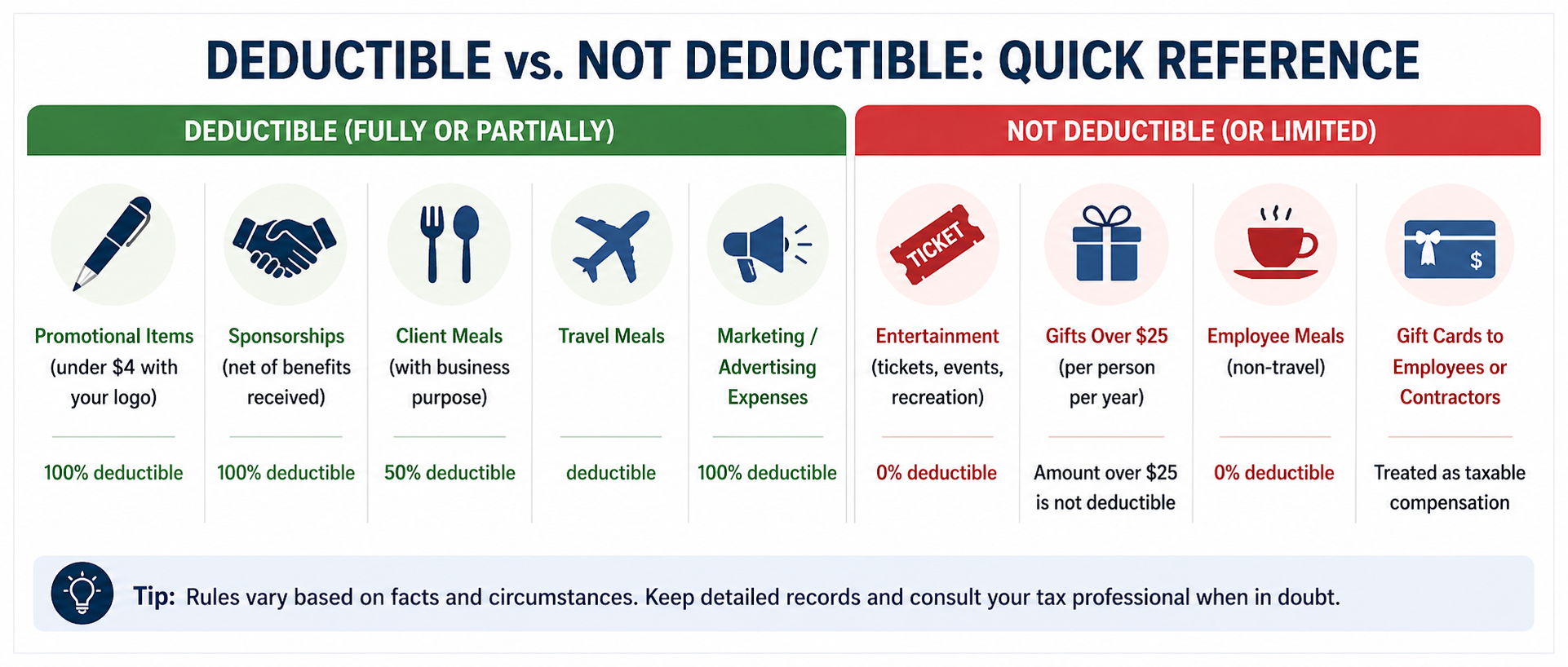

1. What Types of Gifts are Deductible?

The IRS allows businesses to expense $25 per recipient each year as a gift. Let’s say that you send your clients holiday baskets each year and they cost $30. Only $25 of the $30 is tax-deductible. It’s also important to note that incidental costs, such as engraving or packaging, aren’t included in the $25 limit. Using our above example, let’s say that it costs $10 to ship each gift basket, bringing the total cost to $40. You would be able to deduct $25 as a gift and $10 as shipping. The remaining $5 would be non-deductible.

One clarification for 2026: gifts given to spouses of clients are generally treated as being given to the client, so the $25 limit still applies in total.

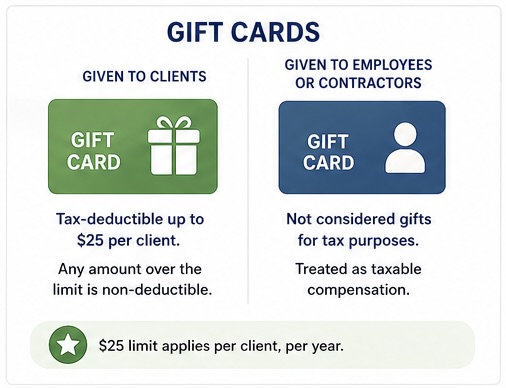

2. Are Gift Cards Tax Deductible?

Gift cards given to business clients are tax-deductible up to the $25 limit per client. Any amount over this limit is non-deductible. Gift cards given to employees or contractors are not considered gifts for tax purposes. They are treated as taxable compensation and should be included in payroll or contractor payments.

3. What Types of Gifts are Considered Promotional?

Promotional and marketing expenses aren’t subject to the $25 limit per recipient. If the value of the item is less than $4, has your business information permanently branded, and is widely available, the item is considered promotional and fully deductible. Think office pads, pens, water bottles, tissues, branded bags, and similar items. These are fully deductible as marketing or advertising expenses.

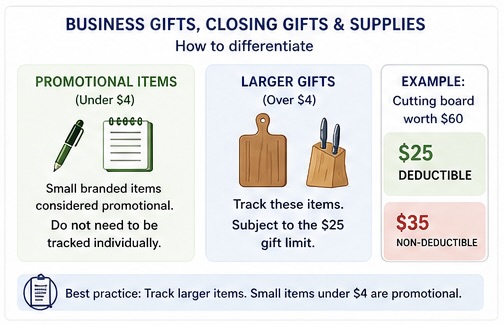

4. Business Gifts, Closing Gifts, and Supplies: How Can You Differentiate?

Differentiating between deductible and non-deductible expenses can be confusing. Let’s say that you have a supply setup where clients can choose items for a closing gift. Some items are small branded items like pens and paper, while others are larger gifts like cutting boards or cutlery.

Best practice is to track the larger items. Smaller branded items under $4 are considered promotional and do not need to be tracked individually. However, larger items should be tracked for gifting limitations.

For example, if you choose a cutting board worth $60, you would note for tax purposes that only $25 is deductible and $35 is non-deductible.

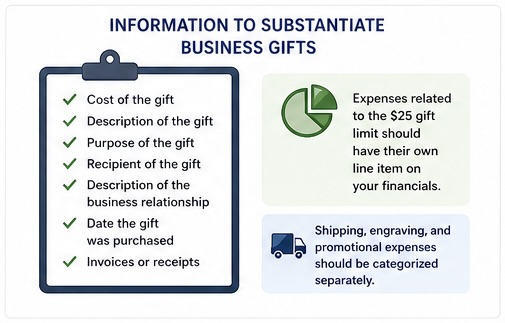

5. What Information is Needed to Substantiate Business Gifts?

If the IRS reviews large gift expenses, they may request support. At a minimum, you should have the following information available:

- Cost of the gift

- Description of the gift

- Purpose of the gift

- Recipient of the gift

- Description of the business relationship

- The date the gift was purchased

- Any applicable invoices or receipts

Expenses related to the $25 business gift limit should have their own line item on your financials. Shipping, engraving, and promotional expenses should be categorized separately.

6. Which is More Tax Advantageous: Making Direct Donations or a Sponsorship?

Both sponsorships and direct donations to qualifying 501(c)(3) charities may be deductible, but they are treated differently.

Sponsorships that provide advertising or marketing exposure (such as your logo displayed at an event) are generally treated as advertising expenses and are fully deductible. Donations without a direct business benefit are subject to charitable contribution rules and AGI-based limitations, depending on your tax situation.

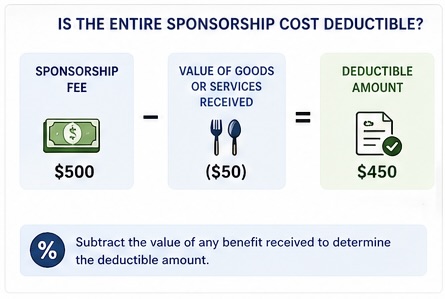

7. Is the Entire Sponsorship Cost Deductible?

Sponsorship deductibility depends on the value of goods and services received. For example, if you sponsor a golf tournament for $500 and receive a meal valued at $50, only $450 may be deductible. The value of the benefit received must be removed from the deductible portion.

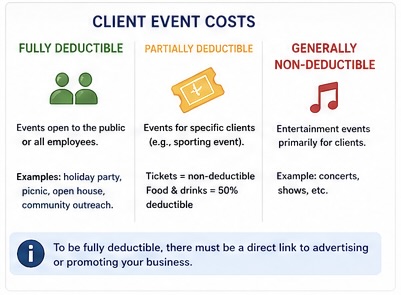

8. What Type of Client Event Costs are Deductible?

The deductibility of client events varies based on the type of event. Generally, entertainment events are considered non-deductible. However, full staff events and events open to the public, like a holiday party, picnic, community outreach, or open house, are fully deductible. To claim full deductibility, you must be able to claim a direct advertising or promotion link.

Events for specific clients, such as taking a handful of clients to a sporting event, are not fully deductible. The cost of the sporting event tickets would be non-deductible as entertainment, while any food and drinks would be subject to a 50% limit.

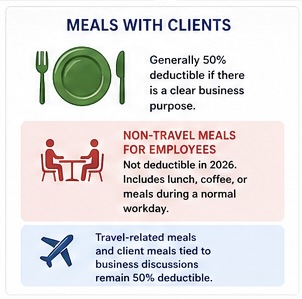

9. Are All Meals with Clients Deductible?

Meals with clients are generally 50% deductible if there is a clear business purpose.

As of 2026, non-travel meals for employees are not deductible. This includes situations like buying lunch or coffee for yourself or your staff during a normal workday. Travel-related meals and client meals tied to business discussions remain 50% deductible.

10. Do You Need to Keep Meal Receipts?

Yes, it is best practice to keep meal receipts. You can maintain digital copies in a secure folder.

For client expenses and events, it is especially important to retain receipts and documentation to support deductibility, particularly when claiming partial or full deductions.